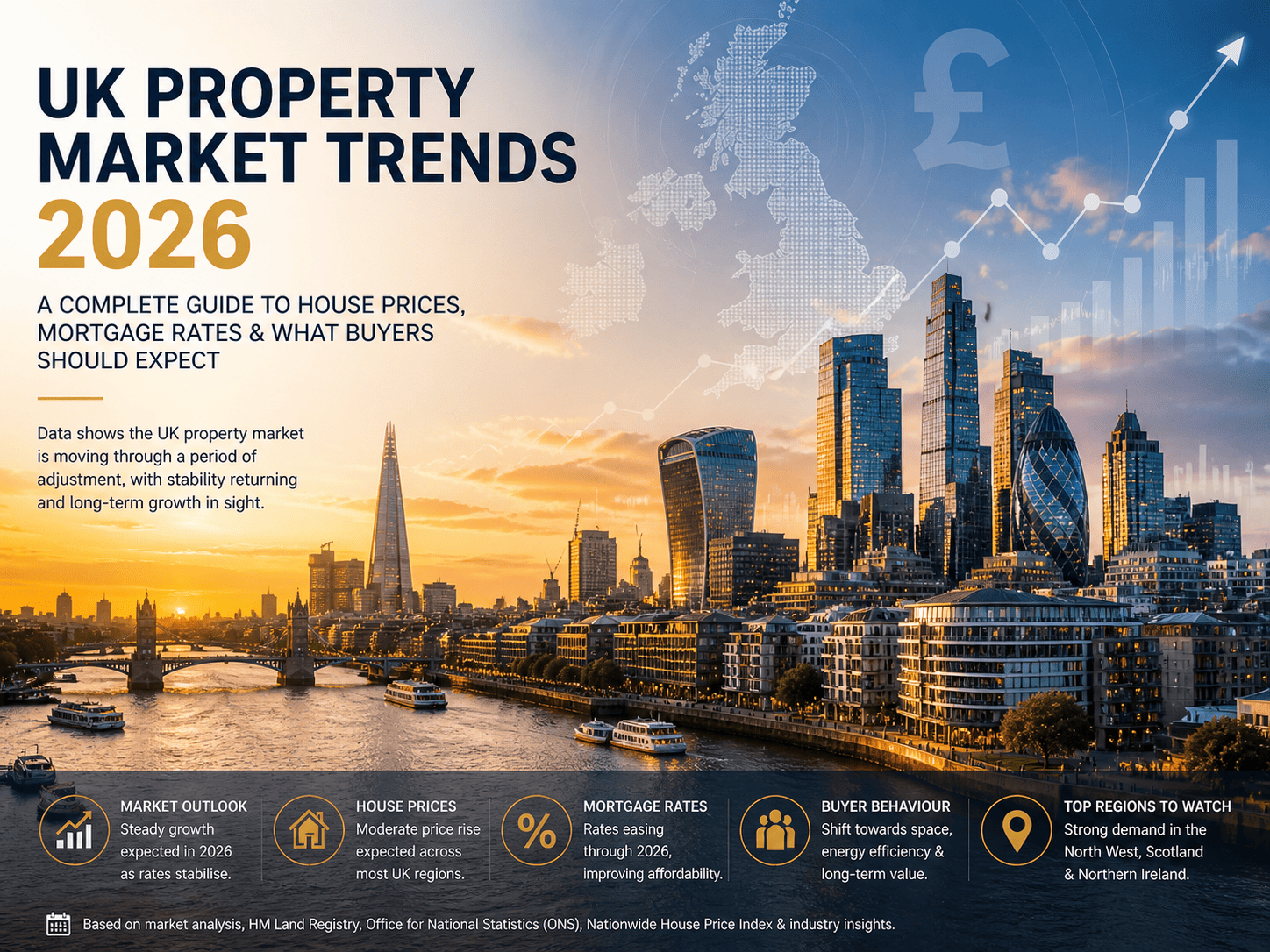

UK Property Market Trends 2026: Complete Analysis

Understanding the UK Property Market in 2026

The UK property market in 2026 is not behaving in extremes—and that’s exactly what makes it interesting. For anyone looking to buy, sell, or invest, the question is no longer “Is the market going up or down?” Instead, it has become: “How is the market evolving, and what does that mean for me?”

Over the past 12 months, the market has moved through a phase of adjustment. Rising borrowing costs, global uncertainty—including the ongoing middle east conflict—and shifting buyer priorities have all played a role. And to understand it properly, we need to look at what the data actually shows.

Experts suggest a "wait and see" approach for the immediate market, with potential for improved affordability and higher transaction volumes later in 2026 as mortgage rates stabilize. The five-year outlook remains positive with expected growth in some areas.

January 2026 to February 2026: A Market Finding Its Balance

At the start of January 2026, activity in the UK property market carried a cautious sense of optimism. Mortgage approvals had begun to stabilise, and there was early confidence that borrowing conditions might improve.

However, by February 2026, the tone shifted slightly. Data shows:

- A slowdown in buyer enquiries

- Slight hesitation in mortgage approval rates

- More negotiation between buyers and sellers

This wasn’t a sudden downturn—it was a sign that buyers were becoming more measured.

People were still interested in moving, but they were taking longer to decide, comparing deals more carefully, and ensuring affordability before committing.

House Prices: Stability Over Rapid Growth

When looking at house prices in 2026, one thing becomes clear—this is no longer a fast-moving market.

According to the latest insights from the HM Land Registry and the Office for National Statistics, the average UK house price has shown only modest changes.

Rather than sharp increases, the trend reflects:

- Minor monthly fluctuations

- Small regional price rise differences

- Overall stability across the UK

The UK house price index indicates that while prices have not fallen dramatically, they are also not accelerating at previous rates. This balance is important.

It means:

Buyers are no longer under pressure to rush

Sellers need to price more realistically

The market is becoming more sustainable

UK Property Market Shift (2024–2026)

To better understand how things have changed, here’s a structured comparison:

| Market Factor | 2024 | 2025 | 2026 Trend |

| Average House Prices | Rising Fast | Slowing | Stable |

| Mortgage Rates | Low–Moderate | Rising | High but Stabilising |

| Buyer Demand | Strong | Cooling | Selective |

| Mortgage Approval | High | Moderate | Cautious |

| Investor Activity | Aggressive | Reduced | Strategic |

This clearly shows that 2026 is not a weak market—it’s a more controlled one.

Mortgage Rates & Affordability: The Real Pressure Point

If there’s one factor shaping the market more than any other, it’s mortgage rates.

Borrowing costs have remained elevated due to global economic conditions, inflation pressures, and policy decisions by the Bank of England.

For buyers, this has a direct and noticeable impact.

A small increase in interest rates can significantly raise monthly payments.

This means affordability is now the central concern for most households.

What’s interesting is how this is changing behaviour.

Buyers are:

- Choosing smaller properties

- Moving further from city centres

- Taking longer to finalise decisions

This shift is subtle, but it is reshaping demand across the UK.

Mortgage Rates vs House Prices

The relationship is clear:

As borrowing becomes more expensive, price growth slows—but remains stable.

Regional Trends: A Market Split Across the UK

The UK property market is no longer moving as one.

Different regions are experiencing different levels of demand and price movement.

Northern Growth Areas

Regions like the north west and Northern Ireland continue to attract strong interest. This is driven by:

- Lower entry prices

- Better affordability

- Strong rental demand

Cities in these regions are becoming increasingly attractive to both first-time buyers and investors.

Southern Market Adjustment

In contrast, higher-priced areas—particularly in and around London—are experiencing slower growth.

This doesn’t mean decline.

It simply reflects:

Affordability limits

Higher mortgage costs

More selective buyers

Stamp Duty & Buyer Psychology

Another important factor influencing behaviour is stamp duty.

Even small changes or thresholds can impact decision-making.

In 2026, buyers are:

- Timing purchases more carefully

- Calculating total costs more precisely

- Looking for value rather than urgency

This has contributed to a market where transactions are slower—but more considered.

What Buyers Are Really Thinking in 2026

To understand the market, it helps to think like a buyer. In previous years, urgency drove decisions. In 2026, it’s caution. Buyers are asking:

- Can I afford this long-term?

- Will rates go down?

- Is this the right time?

This mindset is creating a more stable environment. It reduces risk—but also slows activity.

Properties Reflecting Current Demand

- https://indextoscale.com/property_detail/14a-water-lane-london-united-kingdom-tw9-1tj/

- https://indextoscale.com/property_detail/20-cliffhouse-avenue-london-united-kingdom-me12-2ge/

- https://indextoscale.com/property_detail/15-grebe-close-london-united-kingdom-e7-9ru/

- https://indextoscale.com/property_detail/30a-neville-road-london-united-kingdom-e7-9qx/

- https://indextoscale.com/property_detail/175-boleyn-road-london-united-kingdom-e7-9qh/

Looking ahead, the next 12 months are expected to be defined by gradual improvement rather than dramatic change.

Most forecasts suggest:

- Mortgage rates may stabilise or slightly decline

- Buyer confidence may return slowly

- Prices will remain steady with minor growth

This points toward a soft recovery phase.

The UK property market in 2026 is not driven by hype or fear. It is driven by balance.

- Prices are steady

- Buyers are informed

- Lending is cautious